Paul Krugman

An introduction to my life and publications:

Introduction:

Hello, my name is Paul Krugman A.K.A Krugtron the invincible. I am the professor of economics and international affairs at the Woodrow Wilson school of public and international affairs at Princeton University and an op-ed columnist is the New York times magazine.

Early life:

I was born on February 28th 1953 in New York. My mothers name is Anita Krugman and my father is David Krugman. I graduated from John F. Kennedy high school. I earned my Bachelor degree in economics from Yale university in 1974 and later earned my PhD in the Massachusetts institution of technology in 1977. I had married twice, first to Robin L. Bergman who was an award-winning designer/artist and secondly to Robin Wells who helped me write some of my works.

My interest in economics started when I was a teenager reading Iaac Asimov's Foundation novels, I too wanted to be a protector of and all of civilization/predictor of the future using psycohistory (an imaginary branch of maths which predicts the actions that will be made by populations) but unfortunately there is no such thing as psycohistory but the next best thing was economics.

Notable achievements and famous writings:

I had won the John Bates Clark medal (1991), The Principe de Asturias Prize (2004) and the Nobel prize in economics (2008)

My most famous economic was the new trade theory which had won me the Nobel prize in economics which explains the dynamics of trade between countries.

I have also written a variety of books such as the 'New Economy' (which discusses the growing income inequality gap in America.

My book 'the great unraveling' talked about the unsustainable policies implemented by the Bush administration such as tax reduction on the rich, increased public spending and fighting the Iraq war and that these policies would lead to a major economic crisis.

The 'conscience of a liberal' covers the income gap between the poor and the rich in the 20th century.

Also my book 'End this depression now!' argues that fiscal cuts and austerity measures is not the way to solve the economic crisis.

Here's a video which includes some of my back story:

Hello, my name is Paul Krugman A.K.A Krugtron the invincible. I am the professor of economics and international affairs at the Woodrow Wilson school of public and international affairs at Princeton University and an op-ed columnist is the New York times magazine.

Early life:

I was born on February 28th 1953 in New York. My mothers name is Anita Krugman and my father is David Krugman. I graduated from John F. Kennedy high school. I earned my Bachelor degree in economics from Yale university in 1974 and later earned my PhD in the Massachusetts institution of technology in 1977. I had married twice, first to Robin L. Bergman who was an award-winning designer/artist and secondly to Robin Wells who helped me write some of my works.

My interest in economics started when I was a teenager reading Iaac Asimov's Foundation novels, I too wanted to be a protector of and all of civilization/predictor of the future using psycohistory (an imaginary branch of maths which predicts the actions that will be made by populations) but unfortunately there is no such thing as psycohistory but the next best thing was economics.

Notable achievements and famous writings:

I had won the John Bates Clark medal (1991), The Principe de Asturias Prize (2004) and the Nobel prize in economics (2008)

My most famous economic was the new trade theory which had won me the Nobel prize in economics which explains the dynamics of trade between countries.

I have also written a variety of books such as the 'New Economy' (which discusses the growing income inequality gap in America.

My book 'the great unraveling' talked about the unsustainable policies implemented by the Bush administration such as tax reduction on the rich, increased public spending and fighting the Iraq war and that these policies would lead to a major economic crisis.

The 'conscience of a liberal' covers the income gap between the poor and the rich in the 20th century.

Also my book 'End this depression now!' argues that fiscal cuts and austerity measures is not the way to solve the economic crisis.

Here's a video which includes some of my back story:

My economic theories and ideas:

Introduction:

I would like to start of by saying that I am a Keynesian economist and I do believe that the government indeed has an important role in the economy and must steer the economy when needed.

My opinions on the topics of the great economist debate part 2:

1. What is the proper role of the government in the economy: Well as I had stated in my introduction I do believe that governments must intervene in an economy when needed. Governments must intervene in order to reduce the effects of negative externatlities as there are many situations where there is no private incentive to do what will benefit society. An example of this would be when a farmer uses pesticides near a river, this of course would have a large negative externality to those who live nearby the river but there is no incentive for the farmer to make use of more expensive organic fertilizers to reduce the pollution of the river and so this is where the government must step in.

Of course many of those butt head racist southerners in cowboy hats riding horses everywhere which no one can ever understand when they speak due to their poor speaking skills and many members of the right wing (which have few differences from the former) would tell you that the government is always the problem but they are completely wrong and should go away. (out of character note: I am not being racist myself to southerners this is merely an exaggeration of Paul Krugman's habit of making generalizations in a sarcastic manner in order to get a point across.)

Here I comment on the role of the government:

http://www.nytimes.com/2014/04/28/opinion/krugman-high-plains-moochers.html?rref=opinion&module=ArrowsNav&contentCollection=Opinion&action=click®ion=FixedLeft&pg

http://krugman.blogs.nytimes.com/2009/02/25/what-should-government-do-a-jindal-meditation/?_php=true&_&_r=0

2. Is inequality a major obstacle to growth: Inequality is certainly a major obstacle to economic growth and it is also a major obstacle to growth. It is extremely damaging for an economy to have a large concentration of wealth in the top percentile as the top percentile of an economy will often spend proportionally smaller amount relative to their income compared to the middle class and so demand will fall as inequality increases. Often the richest percentile of an economy will not only spend a small percent of their income but their spending largely consists of investments on securities, bonds and so on, all of which give large returns with and are charged low taxes, this will inevitably lead to a snowball effect in the distribution of wealth which is very harmful to an economy as there will be an overall fall in demand as the middle classes share of the total wealth in the economy falls.

I talk more about inequality and why it matters on my blog:

http://www.nytimes.com/2013/12/16/opinion/krugman-why-inequality-matters.html

3. Governments should always stay with ma certain range of GDP to dept ratio and under no circumstances should they exceed it: I believe that the dept ceiling is a fictional and stupid thing. The government must follow their financial obligations even if it means exceeding this limit especially when it comes to paying off federal deficit as defaulting would lead to a fall in the countries bonds leading to higher interest rates and defaulting because a government is unwilling to cross this imaginary line would be a silly sacrifice.

Here is an article regarding my opinion on the budget deficit:

http://www.huffingtonpost.com/2013/01/13/paul-krugman-debt-ceiling_n_2467718.html

Here is a video of a debate between me and David Brooks:

I would like to start of by saying that I am a Keynesian economist and I do believe that the government indeed has an important role in the economy and must steer the economy when needed.

My opinions on the topics of the great economist debate part 2:

1. What is the proper role of the government in the economy: Well as I had stated in my introduction I do believe that governments must intervene in an economy when needed. Governments must intervene in order to reduce the effects of negative externatlities as there are many situations where there is no private incentive to do what will benefit society. An example of this would be when a farmer uses pesticides near a river, this of course would have a large negative externality to those who live nearby the river but there is no incentive for the farmer to make use of more expensive organic fertilizers to reduce the pollution of the river and so this is where the government must step in.

Of course many of those butt head racist southerners in cowboy hats riding horses everywhere which no one can ever understand when they speak due to their poor speaking skills and many members of the right wing (which have few differences from the former) would tell you that the government is always the problem but they are completely wrong and should go away. (out of character note: I am not being racist myself to southerners this is merely an exaggeration of Paul Krugman's habit of making generalizations in a sarcastic manner in order to get a point across.)

Here I comment on the role of the government:

http://www.nytimes.com/2014/04/28/opinion/krugman-high-plains-moochers.html?rref=opinion&module=ArrowsNav&contentCollection=Opinion&action=click®ion=FixedLeft&pg

http://krugman.blogs.nytimes.com/2009/02/25/what-should-government-do-a-jindal-meditation/?_php=true&_&_r=0

2. Is inequality a major obstacle to growth: Inequality is certainly a major obstacle to economic growth and it is also a major obstacle to growth. It is extremely damaging for an economy to have a large concentration of wealth in the top percentile as the top percentile of an economy will often spend proportionally smaller amount relative to their income compared to the middle class and so demand will fall as inequality increases. Often the richest percentile of an economy will not only spend a small percent of their income but their spending largely consists of investments on securities, bonds and so on, all of which give large returns with and are charged low taxes, this will inevitably lead to a snowball effect in the distribution of wealth which is very harmful to an economy as there will be an overall fall in demand as the middle classes share of the total wealth in the economy falls.

I talk more about inequality and why it matters on my blog:

http://www.nytimes.com/2013/12/16/opinion/krugman-why-inequality-matters.html

3. Governments should always stay with ma certain range of GDP to dept ratio and under no circumstances should they exceed it: I believe that the dept ceiling is a fictional and stupid thing. The government must follow their financial obligations even if it means exceeding this limit especially when it comes to paying off federal deficit as defaulting would lead to a fall in the countries bonds leading to higher interest rates and defaulting because a government is unwilling to cross this imaginary line would be a silly sacrifice.

Here is an article regarding my opinion on the budget deficit:

http://www.huffingtonpost.com/2013/01/13/paul-krugman-debt-ceiling_n_2467718.html

Here is a video of a debate between me and David Brooks:

4. Should central banks raise and lower interest rates in order to expand and contract demand: Yes I do think that the central bank is the most equipped institution to steer the economy for the better.

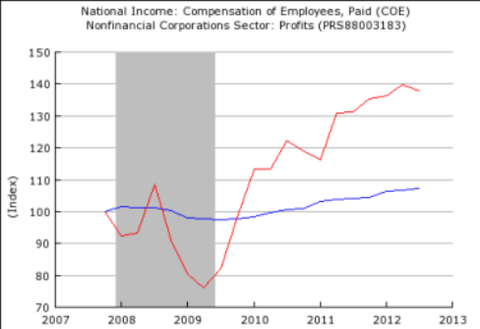

5. Trickle Down economics is the best way to stimulate long term growth: In my opinion this is completely not the case, simply put this idea is made by a group of very serious people who are refuse to read econs 101. The simple fact is that the average workers wage does not vary with the changes in corporate earnings and the earnings of the top richest percentile simply because, as said before, the richest top percentile save more then they spend. Here is a graph showing how workers earnings (represented by the blue line) and corporate earnings (represented by the red line):

5. Trickle Down economics is the best way to stimulate long term growth: In my opinion this is completely not the case, simply put this idea is made by a group of very serious people who are refuse to read econs 101. The simple fact is that the average workers wage does not vary with the changes in corporate earnings and the earnings of the top richest percentile simply because, as said before, the richest top percentile save more then they spend. Here is a graph showing how workers earnings (represented by the blue line) and corporate earnings (represented by the red line):

6. Economics would be better off without central banks and currency controls, markets should be self correcting: No This is simply not possible as central banks are an essential component of an economy and must be kept in order to steer the economy.

7. Should central banks aim for 0% inflation?: This is simply impossible and in fact can be very dangerous as aiming for very low inflation can easily lead to deflation which causes many more problems. A good analogy of 0% inflation would be trying to put a ball on the peak of a mountain, the ball can so easily fall in either way with the slightest gush of wind.

8. Tax rates should be heavily progressive, taking from the rich to supplement social programs: A heavily progressive tax would be necessary in order to combat the high inequality in today's economy but I believe that such spending should be focused on government spending in order to increase the middle class' share of the wealth which will increase demand as the middle class is the biggest driving force in the economy however I do believe that governments should supplement social programs as well.

9. Should governments exert more control or less over the finance sector?: I believe that governments should control financial sectors as deregulation was one of the major causes of the financial crisis in 2008 and the savings-and-loan crisis of the 1980's as deregulations encourages the financial sector to make more and more risky investments which could lead to a financial crisis.

10. Do governments have a reason to keep the gold reserve?: I don't believe it is a good idea as gold is not a safe investment as some may say as much of the time there are fluctuations in price like in the 70's when the price had fallen by more than two-thirds.

Here I comment on investing in gold:

http://www.nytimes.com/2013/04/12/opinion/krugman-lust-for-gold.html

Comments:

Raghuram Rajan- So we meet again Krugman. I think you should move on from your narrow pro-Keynesian views on government intervention in the economy. The government can only do so much in the economy, don't you think that it is greatly up to the nation to affect the economy as well? Essentially, the economy is affected by the behaviour of consumers and labour of a nation, therefore, structural and supply-side reforms play a more vital role as government intervention is not always feasible.

7. Should central banks aim for 0% inflation?: This is simply impossible and in fact can be very dangerous as aiming for very low inflation can easily lead to deflation which causes many more problems. A good analogy of 0% inflation would be trying to put a ball on the peak of a mountain, the ball can so easily fall in either way with the slightest gush of wind.

8. Tax rates should be heavily progressive, taking from the rich to supplement social programs: A heavily progressive tax would be necessary in order to combat the high inequality in today's economy but I believe that such spending should be focused on government spending in order to increase the middle class' share of the wealth which will increase demand as the middle class is the biggest driving force in the economy however I do believe that governments should supplement social programs as well.

9. Should governments exert more control or less over the finance sector?: I believe that governments should control financial sectors as deregulation was one of the major causes of the financial crisis in 2008 and the savings-and-loan crisis of the 1980's as deregulations encourages the financial sector to make more and more risky investments which could lead to a financial crisis.

10. Do governments have a reason to keep the gold reserve?: I don't believe it is a good idea as gold is not a safe investment as some may say as much of the time there are fluctuations in price like in the 70's when the price had fallen by more than two-thirds.

Here I comment on investing in gold:

http://www.nytimes.com/2013/04/12/opinion/krugman-lust-for-gold.html

Comments:

Raghuram Rajan- So we meet again Krugman. I think you should move on from your narrow pro-Keynesian views on government intervention in the economy. The government can only do so much in the economy, don't you think that it is greatly up to the nation to affect the economy as well? Essentially, the economy is affected by the behaviour of consumers and labour of a nation, therefore, structural and supply-side reforms play a more vital role as government intervention is not always feasible.